Last year's venture capital landscape was marked by a significant $141B+ in total venture-backed exits, yet beneath this success lies a serious financial burden for startup founders. Data from the Hercules Capital 2025 Market Report revealed that while total exit value reached new heights, a vast majority of founders likely lost a substantial portion of their gains to federal taxes after missing out on the benefits of the Qualfiied Small Business Stock exclusion.

Our estimates suggest that founder proceeds from these exits ranged between $21B and $50B. However, because approximately 71% of these exits occurred at or before the Series A stage (which we use as a proxy for a holding period of less than five years) most shareholders failed to meet the mandatory threshold for the QSBS tax exemption. Consequently, an estimated $5B to $13B was lost to taxes in 2025 alone, money that essentially evaporated from the startup economy simply because the five-year holding requirement was not met.

To grasp the magnitude of this $13B loss, it’s helpful to look at the purchasing power that disappeared from founders' hands. This amount of capital lost is equivalent to the total value of major market players like Airtable, Whatnot, Kalshi, Notion, or Gusto. On an institutional level, $13B is enough to surpass the AUM of large venture capital firms like Lightspeed, Kleiner Perkins, Greylock, and others.

Perhaps most shockingly, this tax money alone could have been used to take any one of more than 3,000 of the US’s publicly-listed companies private. Rather than being reinvested to fuel further innovation and growth, this capital was diverted to the treasury, representing a massive missed opportunity for compounding value within the private sector.

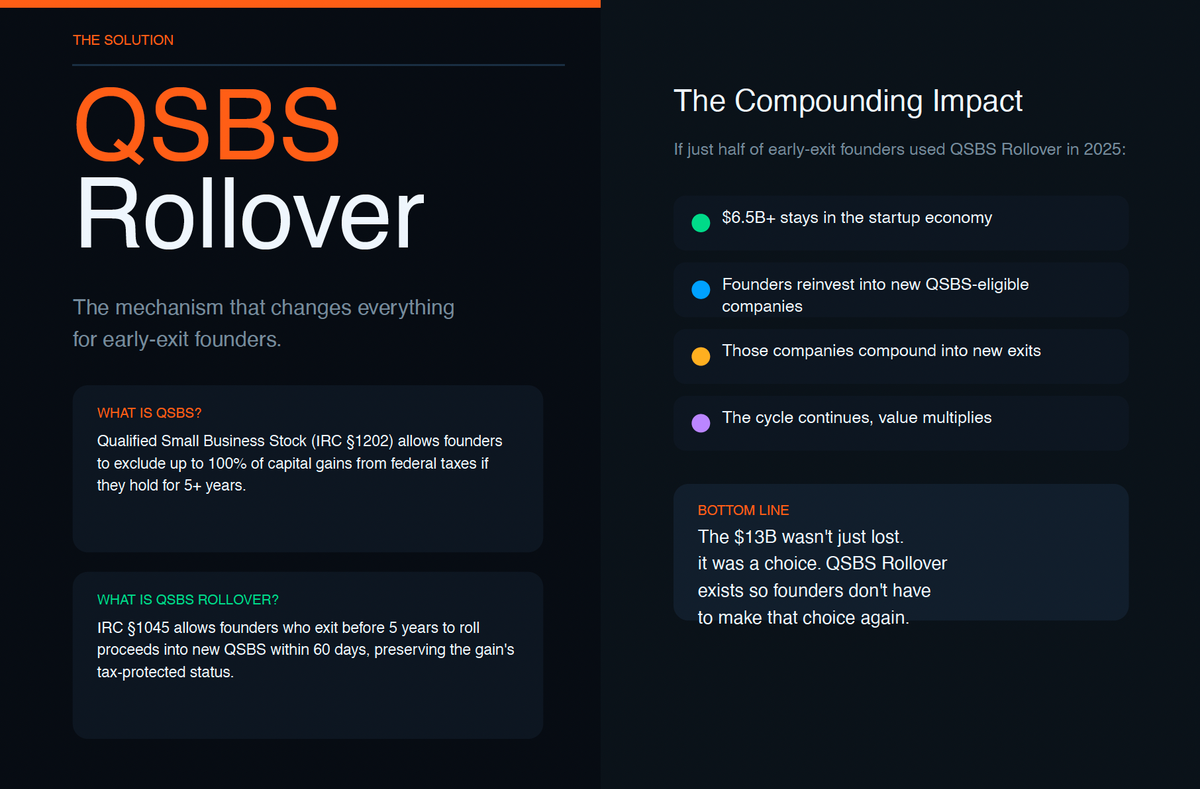

Fortunately, this financial drain is not an unavoidable cost of an early exit, but rather a choice that can be managed through the use of QSBS rollovers. While IRC §1202 normally requires a five-year hold to exclude up to 100% of capital gains, IRC §1045 provides a critical mechanism for those who exit earlier. By utilizing a QSBS rollover, founders have a 60-day window to reinvest their proceeds into new QSBS-eligible companies, effectively preserving the tax-protected status of their gains and allowing the five-year "clock" to continue.

If even half of the founders who exited early in 2025 had utilized this rollover strategy, over $6.5B would have remained in the startup ecosystem to compound into new ventures and future exits. The QSBS rollover exists specifically so that founders do not have to choose between a timely exit and tax efficiency, ensuring that the wealth created by startups stays where it can have the most impact: in the hands of founders.