Qualified Small Business Stock (QSBS) offers significant tax advantages to founders, but the rules governing its treatment under the Internal Revenue Code can be complex. This guide provides Certified Public Accountants (CPAs) with a comprehensive overview of the filing procedures and compliance requirements for QSBS, focusing on the Section 1202 gain exclusion and the Section 1045 rollover. A clear understanding of these provisions is essential for CPAs to effectively advise their clients and ensure compliance with tax laws.

This guide will address the common misconception regarding the use of Form 1045 in the context of QSBS and will clarify the proper use of Form 8949 and Schedule D in reporting these transactions. By the end of this guide, CPAs will have a clear roadmap for navigating the intricacies of QSBS tax reporting.

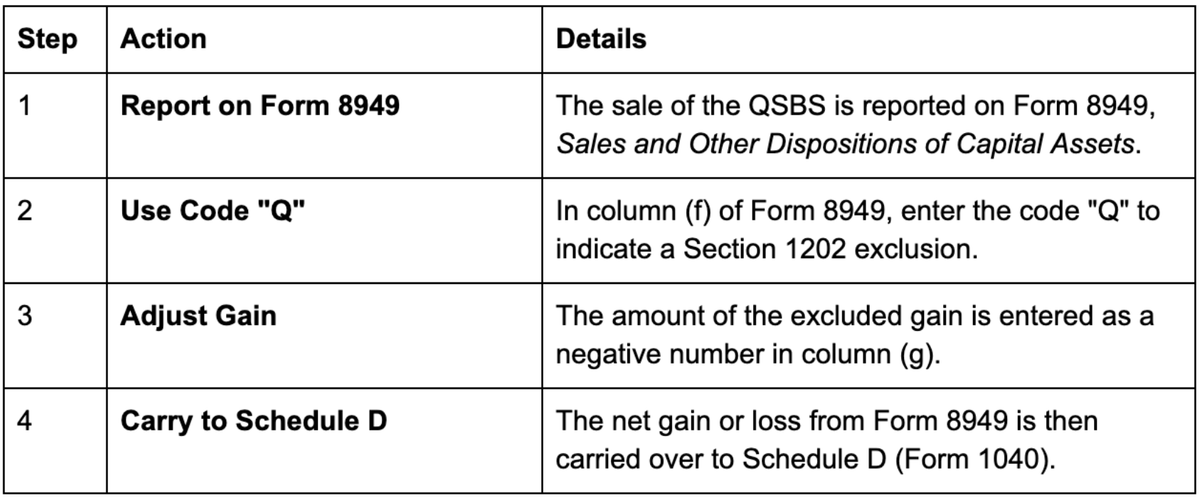

Section 1202 of the Internal Revenue Code allows taxpayers to exclude a significant portion of the gain from the sale of QSBS. For stock acquired after September 27, 2010, the exclusion is 100% of the gain, subject to certain limitations.

The process for claiming the Section 1202 exclusion is as follows:

To ensure compliance, CPAs must verify that the following requirements are met:

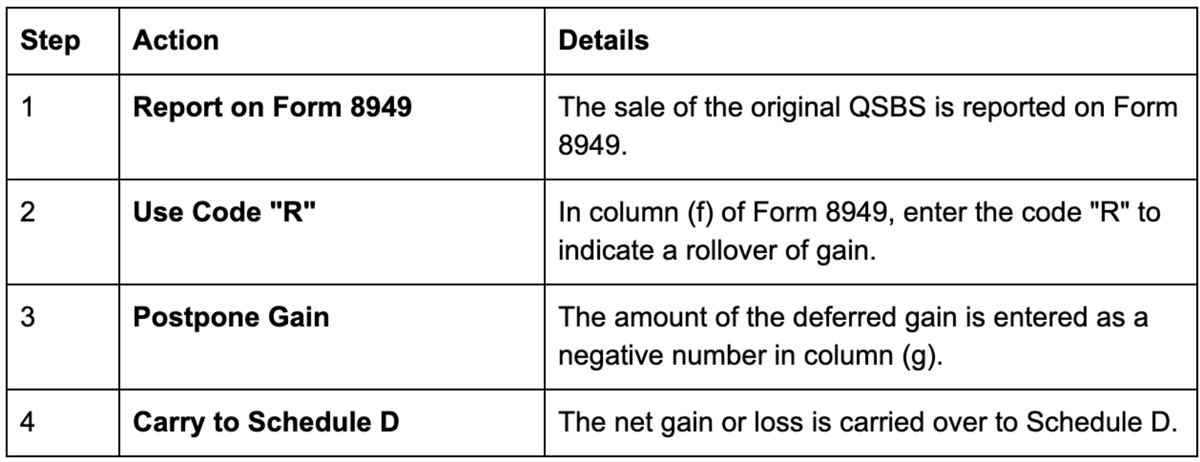

Section 1045 provides a valuable tax-deferral strategy for QSBS held for more than six months but less than the five years required for the Section 1202 exclusion. This allows investors to roll over the gain from the sale of QSBS into new QSBS, deferring the tax liability.

The filing process for a Section 1045 rollover is similar to that of the Section 1202 exclusion:

For a successful Section 1045 rollover, the following conditions must be met:

A common point of confusion for CPAs is the role of Form 1045, Application for Tentative Refund. It is important to note that Form 1045 is not used for Section 1045 QSBS rollovers. This form is intended for carrybacks of net operating losses (NOLs) and certain other credits. The Section 1045 QSBS rollover is an election made on Form 8949 and Schedule D, not an application for a refund on Form 1045.

CPAs can leverage the interplay between these two sections to their clients' advantage:

Properly navigating the tax implications of QSBS requires a detailed understanding of both Section 1202 and Section 1045. By following the procedures outlined in this guide, CPAs can help ensure compliance, avoid common pitfalls, and provide valuable tax-planning advice to their clients. The key takeaways are to use the correct forms (Form 8949 and Schedule D), the correct codes ("Q" for exclusion, "R" for rollover), and to maintain meticulous documentation for all QSBS transactions.